Highlights

- The Impeachment Trial for President Trump begins today in the Senate, President Trump will be at the World Economic Forum in Davos.

- President Trumps approval percentage among rural voters is at the highest level, according to Farm Journals latest poll.The new rating is at 83% of the 1,286 respondents.

- Secretary of Ag Sonny Perdue confirmed the 3rd round of MFP 2.0 payments will be coming, but not to expect a MFP 3.0.

- Brazilian soybean harvest is at 1.8% complete, a late start to harvest is the residual affects of the late planting season they endured. Very early yields point to another big crop.

- Weekly USDA export inspections report out at 10 a.m. central time.

- Cattle on Feed report is out this Friday.

Corn

- The corn market saw weaker overnight markets after the long weekend and strong day last Friday.

- Anticipation remains that the U.S. will see more demand from China after the dust has settled from the Phase 1 signing, whether that is DDG or ethanol imports.

- One thought out there is that China could fulfill its Tariff Rate Quotes as outline by the WTO.If that were true, that could turn into 7.2 MMT of corn imports (The USDA currently estimates Chinese corn imports at 7.0 MMT).

- Some concern is growing about dryness in the corn growing areas of Brazil, especially towards the effects it could have on the safrinha crop in Mato Grosso which produces 42% of the total second corn crop.Mato Grosso has seen 57% of its normal precipitation the last two weeks.

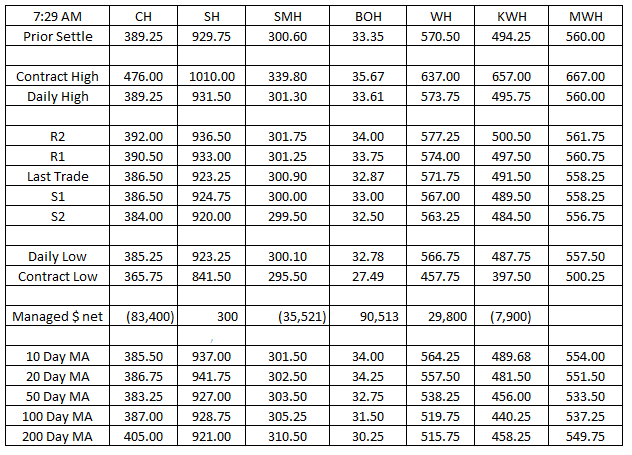

- Funds grew their short position by 12k contracts to put their net short at 121,095 contracts.The largest net short in 5 weeks.

- Spreads: H/K 6 ¼ carry, K/N 5 ¾ carry, N/Z 2 ½ carry.

Outlook: It seems like we will settle back into the ranges the market has been comfortable with since early December, we await some strong news to push the market out of it.

Oilseeds

- Soybeans are seeing a weaker market on the overnight as the market continues to feel a downward trend.

- We await any fresh, and substantial, buying from the Chinese in the spot market.From a price standpoint, we aren’t the cheapest in the world and Brazil is beginning its harvest season with a record crop expected to hit the export pipeline.

- A few sources are thinking the Chinese imports will increase to 90 MMT vs. the USDA estimated of 85 MMT.

- Soybean oil has a weaker feel to start the week, a continued downward turn feels evident.Soymeal has been quite choppy since early December and feels rangebound.

- Funds were buyers of 3.5k contracts last week to cut their new short position to 20,256 contracts for soybeans.Funds are long 90,513 in the soyoil market and short 31,720 in the soymeal market.

- Spreads: H/K 13 ½ carry, H/N 26’0 carry, N/X 6 carry, X/F 3 ½ carry.

Outlook: Until we hear or see fresh demand news out of China or major issues arising with the South American crop, we should see neutral to lower prices.

Wheat

- Feeling the pressure of lower corn and soybean markets, MN and KC teetering on the lower side of things with CHI overall quiet.

- Domestic wheat news remains thin, strong export demand of HRS in the last month is helping with our balance sheets.

- There is hope still that the Chinese will buy U.S. wheat, and if they do, it’s likely it would be HRS.

- Algeria is tendering to buy 50,000 MT of milling wheat.

- Funds are short 5,345 contracts in KC, short 3,515 in MN, and long 6,424 in CHI wheat.

- Spreads: Mpls H/K 8 ½ carry, Kansas City H/K 7 ¼ carry, Chicago H/K 2 ¾. carry.

Outlook: With rallies in the wheat as of late, the market will want to see more news or Chinese buying to keep spurring things higher.